Letter #102: Tom Kamei (2023)

Investor at Counterpoint Global | Investment Culture and Sustainability Research

Today’s letter an essay by written by Tom Kamei, adapted from a talk he gave at Notre Dame. In this letter, Tom discusses the shift from tangible to intangible investments, compares the sustainability wave to the digital wave, sustainability going mainstream, millennials as catalysts, sustainability through a prism, the convergence of profits and purpose, flaws in existing frameworks, measuring externalities, and much more.

Tom is an investor for Counterpoint Global and leads the Sustainability Research integration strategy for the US based funds managed by the team. He was a Fellow at The Aspen Institute in 2015 where he developed a proprietary process to quantify executive compensation alignment. Prior to his current role, Thomas worked with Counterpoint Global for two years as an intern. Previously, he was a research intern at Kleiner Perkins Caufield & Byers where he analyzed late stage private technology businesses for the Green Technology Growth Fund. Thomas received a B.S. in architectural studies from the University of Southern California.

Tom is also one of the most interesting investors out there—he’s an architect by training, a value investor by principle, a tech analyst by practice, and a sustainability researcher by purpose. If you’re wondering how that’s possible, so did I.

The answer is quite simple: He’s been going to the Berkshire Hathaway Annual Meeting every year since 1997, had the pleasure of asking Warren and Charlie several questions (pasted below), and taken their answers (linked) seriously.

TK Berkshire Questions:

2000: My name is Thomas Kamei. I am 10 years old and I go to Bacich School in Kentfield, California. I have been a shareholder for two years. This is my third annual meeting. Here’s my question: I know you won’t invest in technology companies, but are you afraid that the internet will hurt some of the companies that you do invest in, such as The Washington Post or Wells Fargo? Thank you. (Morning Session, Question 5.)

2001: Good morning. My name is Thomas Kamei. I am 11 years old and from Kentfield, California. This is my fourth annual meeting. Last year, I asked how the internet might affect some of your holdings. Since a lot of the internet companies have gone out of business, how are — has your view of internet changed? (Morning Session, Question 15.)

2002: Mr. Buffett and Mr. Munger, my name is Thomas Kamei. I am 12 years old. I live in Kentfield, California. This is my fifth annual meeting.

I know you lost a lot of money as a result of 9/11. But I would like to know how 9/11 changed your life and your investment strategy? (Morning Session, Question 18.)

2007: Good morning. I’m Thomas Kamei from San Francisco. I’m 17-years-old and this is my tenth consecutive annual meeting. Mr. Buffett and Mr. Munger, I’m curious about what you think is the best way to become a better investor. Should I get an MBA? Get more work experience? Read more Charlie Munger Almanacs or merely is it genetic and out of my hands? (Morning Session, Question 14.)

2017: Hi, Warren. This one’s a fun one. Thomas Kamei is here. He’s a 27-year-old shareholder from Kentfield, California. And I should preface this question by saying that he was here 17 years ago at 10 years old, asked you a question from the audience asking you if the internet might hurt some of Berkshire’s investments. At the time, you said you wanted to see how things would play out. He’s now updated the question. “What do you think about the implications of artificial intelligence on Berkshire’s businesses, beyond autonomous driving and GEICO, which you’ve talked about already? In your conversations with Bill Gates, have you thought through which other businesses will be most impacted? “And do you think Berkshire’s current businesses will have a significantly — will have significantly more or less employees a decade from now as a function of artificial intelligence?”(Afternoon Session, Question 13.)

Two decades after asking Warren and Charlie about the internet, and after one decade as an internet analyst, Tom is now focused on sustainability research and investing. He has total conviction that the for-profit mechanism is a powerful lever to unleash humanity’s ingenuity and can help solve society’s most intractable issues while creating trillions of equity value along the way.

I hope you enjoy this essay as much as I did!

Relevant Resources:

Berkshire Hathaway

Warren Buffett Compilation (4,839 pages)

Charlie Munger Compilation (1,041 pages)

Counterpoint Global

Michael Mauboussin Compilation (2,343 pages)

Letter

At Counterpoint Global, we make long-term investments in companies that we believe can realize a significant increase in market value. This value creation is the result of enduring competitive advantages that are stewarded by capable management teams. Our culture combines a partnership mindset with a commitment to continuous learning, intellectual flexibility, and self-awareness. We are willing to be different, when necessary, to increase our advantage. These are also the traits we seek in company management. In our view, executives who make thoughtful decisions that incorporate the needs of all stakeholders create the most lasting value. Our focus on sound practices is resolute, whether in capital allocation, corporate governance, operational excellence, or regulatory capture.

Our study of unique businesses reveals a change in how management teams create value. A railroad is very different from a social media company because physical barriers to entry are unlike network effects. A shift from tangible to intangible investments creates a change in how companies create competitive advantage. Smart management teams recognize this shift and understand what they need to do to pursue profitable growth. We have worked hard to understand these factors as well. As a result, a formalized Sustainability Research framework is now integrated into our investing process.

Sustainability Research is not a separate methodology or exclusive from our core activities. Our approach provides insight to our existing investment process and adds to our anticipated investment returns. Human behavior is anchored on existing processes and relationships and is hard to change. We think this holds true for investors. The implementation of an environmental, social, and governance {ESG) methodology is failing at many investment firms because of the combination of inertia and a lack of understanding.

Counterpoint Global's proprietary method for measuring and evaluating sustainability has led to valuable and expanding conversations with management teams. Most managements appreciate the insights we have gleaned from studying how companies have aligned profits and impact successfully. The result is a valuable dialogue. A deepening of our partnerships with management teams naturally leads to a better understanding of how they make decisions. This gives us a deeper appreciation for the risks and they face. By engaging management teams on sustainability, we signal that we value these efforts for both their long-term value creation potential and their impact on society.

To achieve this convergence of profits and impact, it is important to maintain flexibility and willingness to invent. Otherwise, we will risk being left behind and will be continuously catching up with regulators and competitors. That being said, it is good to understand the current landscape for sustainability investing and how it has evolved.

An Evolving Investment Landscape:

With change comes opportunity. Similar to the digital wave that started around 2010, we view the sustainability wave as a driver for certain companies to benefit significantly.

New technologies spur the creation of new business models, such as rich content delivery supported by ads and software-as-a-service. Some companies capitalized on these changes and created trillions of dollars of equity value. The cultural move toward considering environmental and societal issues is compelling companies to rethink how they differentiate themselves. The ultimate goal is to capitalize on these new markets and opportunities.

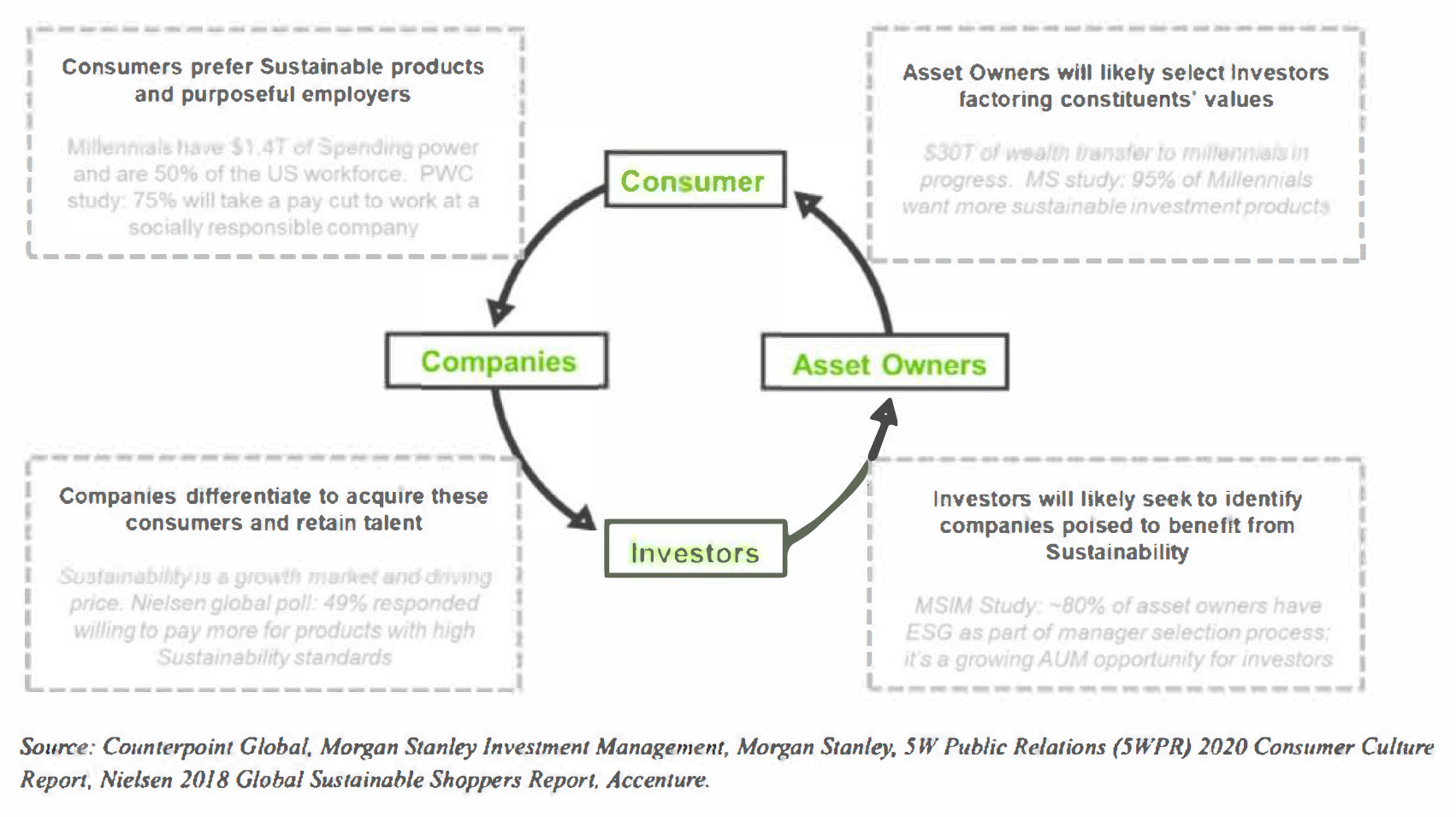

Although sustainability has gone through cycles of optimism over the years, multiple stakeholders are now driving society toward a more sustainable economy. This recent optimism is helping move sustainability investing from the fringe focused on ethics to mainstream asset management. This shift is accelerating and is benefitting from a self-fulfilling cycle.

Looking at the economy through the lens of four key stakeholders-consumers, companies, investors, and asset owners-helps us see the drivers of a more sustainable economy. Let's start with consumers. Millennials are increasingly driving decision making. As a consumer class, millennials have $1.4 trillion of purchasing power and often consider environmental and social factors in their decisions to purchase. Millennials are also more than half of the US workforce and studies show that three-quarters of them are willing to take a pay cut to work at a socially responsible company.

Companies will not only need to offer goods and services that align with these preferences, they will also need to qualify their societal purpose to appropriately attract and retain talent.

Investors should seek and identify those companies that are best positioned to benefit from these themes.

Asset owners, the clients of investors, influence investor behavior and ultimately represent individual consumers. We are currently undergoing the largest wealth transfer in history, with $30 trillion of wealth going to millennials in the coming decades. Millennial investors will drive the progression toward more sustainable considerations in investing. They are expected to allocate their investments in a way that is aligned with their values.

Innovation on Additive Integration:

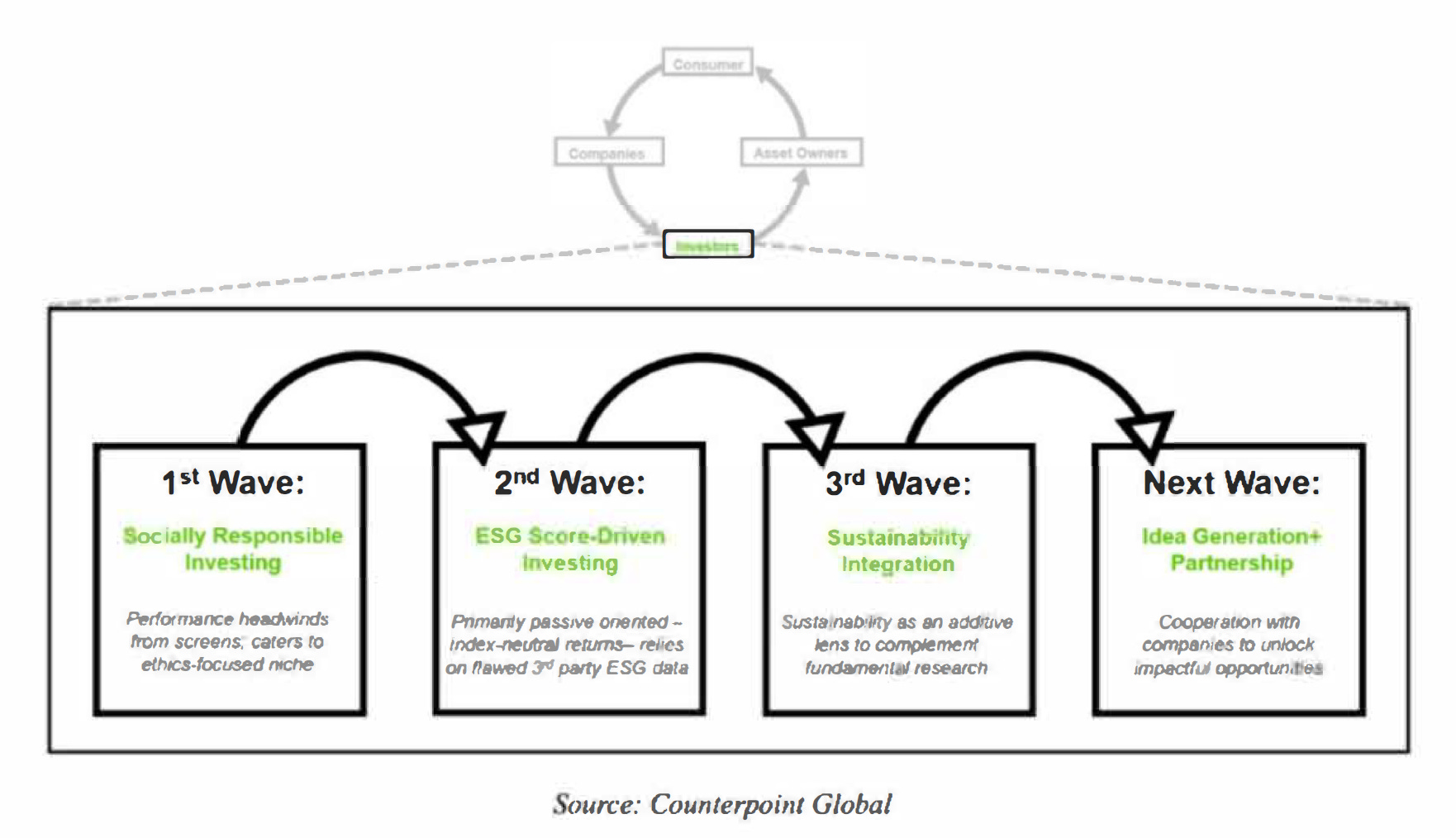

Just as consumer preferences are changing, so too are the practices of investors. We believe the industry is moving away from reductionist screening toward active integration. The first wave of sustainability-oriented investing dates back to the 1960s. Socially Responsible Investing (SRI) was born out of the divestment movement. SRI portfolios did not invest in certain geographies, such as South Africa, or catered to religious organizations by not owning "sin stocks," including companies associated with tobacco, gambling, or weapons. This wave catered to a niche of investors who willingly accepted lower returns to avoid companies they found objectionable. The second wave sought to address the headwind of investment returns. The idea was to create investment services that helped deliver returns similar to the overall market with portfolios that held fewer "bad" companies. These portfolios generally relied on filters that third-party rating agencies created. These filters identified the companies with outsized risk based on exposure to ESG risk factors. This wave has grown to be large but has a fundamental flaw: it is based on rating agencies that create scores based on self-reported and incomplete data. Investment firms still follow this approach, but innovative solutions are rising to meet more demanding standards.

The third wave is Sustainability Integration, which is comprised of asset managers who integrate considerations about sustainability into their analysis. Investors using this approach look to understand sustainability themes in order to add insight into the process of fundamental research. This is something that Counterpoint Global has been doing for years. Integration and Idea Generation enable what the constituents of asset owners want. They do not want fewer "bad" companies but rather more "good" companies. These investors may also be the source of the additional capital necessary to scale solutions that may solve society's more vexing issues.

Whereas the existing ESG landscape takes a reductionist approach, we think the future sees sustainability through a prism. Instead of shrinking the view, it expands it. The environmental and social initiatives that investors identify can create positive and negative options. These options can be material drivers of opportunities or risks for an enterprise.

Our "Value Driver" model complements our investment research process and allows us to evaluate how initiatives based on sustainability build or erode business value. We seek to understand the impact of a company's environmental and social initiatives on its moat, growth, efficiency, optionality, or risk. We have taught our "Value Driver" model to Fellows at the Aspen Institutes' First Movers program for the past five years, which is helping sustainability leaders at the world's leading companies articulate and quantify the business value their initiatives create.

Importantly, the Value Drivers are distinct from Corporate Social Responsibility (CSR). As active investors, we consider a company's environmental and social initiatives that do not drive business value to be part of CSR. Accordingly, we do not include CSR in the valuation of an investment.

Proprietary Quantitative Tools for Integration:

We synthesize our quantitative and qualitative research in our Sustainability Research dashboard (example below) and insights notes. These are published internally for the benefit of our senior investors. These notes capture an analysis of the most material opportunities and risks associated with environmental and societal issues. They also provide an analysis of the alignment between incentives and long-term value creation. Finally, they include an evaluation of a company's cultural adaptability.

For example, our qualitative research may capture how sustainability initiatives can strengthen a durable competitive advantage. These insights come mostly from direct engagement with the company or fundamental research on the investment opportunity. We complement our qualitative research with quantitative tools that rely on unique datasets and processes that we invented. Here are three examples:

People-Focused Quantitative Process: We created our Culture Quant tool in collaboration with academics at Harvard Business School. This uses employee retention to help investors assess the degree to which a company has a "Culture of Adaptability" and engagement. We transformed monthly employment data from Revelio for more than 300 million professionals to develop the tool. We are now using it, along with methods from machine learning, to estimate employment patterns over the coming year.

Planet-Focused Quantitative Process: We developed a proprietary framework for the internalization of emissions in partnership with MIT's Joint Program on the Science and Policy of Global Change. Carbon Internalization estimates the impact of a carbon tax on the profit margins of portfolio companies. The estimate is enabled by our internal risk model and our new Barra profitability factor that is adjusted for intangible value.

Systems-Focused Quantitative Process: We developed a tool to better understand the alignment of long-term incentives while serving as a Fellow at the Aspen Institute in 2015. This tool helps investors visualize the vesting schedules of equity compensation of the top five "Named Executive Officers" of companies.

We share these insights with Counterpoint Global investors through research notes. Our framework allows us to monitor companies on these issues and to identify Sustainability Optionality that the market consensus may misunderstand or underappreciate.

Our Next Evolutionary Step - Internalizing Positive Externalities

Companies across the economy are increasingly investing in intangible capital. Our research into the sustainability strategies of companies finds that positive externalities—the beneficial impact companies are having on people, planet and systems—is a form of intangible value.

The next step for our Sustainability Research process is to invent a method to measure the impact of positive externalities. Pundits outside of investing often criticize sustainability initiatives because the costs and benefits are unknown. While it is difficult to measure the impact of sustainability precisely, we believe the convergence of profits and purpose will lead to improved long-term business performance and investment returns.

Market participants have historically overlooked impact as a form of intangible value because it is difficult to quantify and outcomes are generally not comparable. For example, it is hard to compare removing 3,000 tons of plastic waste from the ocean to economically empowering 3,000 emerging market merchants, even though both are good for the world. We find that the existing frameworks to measure impact are not useful for capital allocators. For instance, we think that the industry's categories of E, S, and G are too broad and reductive. Other frameworks, such as the United Nations Sustainable Development Goals (SDGs), are useful in unifying nongovernmental organization (NGO) development agencies but less applicable to the business world.

Rather than relying on existing frameworks, we decided to propose our own. Our framework is tailored for capital allocators seeking to align impact with value creation. Our approach is based on years of research and hundreds of discussions with companies about how their initiatives drive value. This work allowed us to identify and codify ten types of business activities that benefit society as well as drive financial value. We call these categories Sustainability Research (SR) Tailwinds.

The SR Tailwinds framework improves on other approaches by allowing us to better categorize companies, understand their underlying business activities, and assess the impact of the externalities they produce. This categorization enables us to compare positive externalities more effectively and to see how efficient companies are in producing intangible capital as compared to peers.

Over time, we hope to develop benchmarks on the efficiency of impact. This measure of efficiency can be considered as a component of business quality. As investors start to measure externalities, companies will have an incentive to compete on sustainability initiatives and to scale their practices. This will have a positive impact on society.

Theory of Change:

Historically, businesses have ranked their capital allocation opportunities based primarily on return on invested capital. Think of this as the primary axis. We introduce impact as a source of intangible value that should also be part of capital allocation evaluation. This is a secondary axis. Adding a second axis allows us to visualize a theory of change.

Step 1: Companies embarking on a sustainability journey can start with opportunities that are "low hanging fruit." These investments deliver high tangible returns and significant positive impact.

Step 2: After picking the low hanging fruit, companies considering impact can invest in "win/win" opportunities. These are activities as lucrative as other investment opportunities but have the additional benefit of delivering meaningful positive outcomes for society.

Step 3: Organizations that gain experience in evaluating impact can identify "white whale" opportunities. These initiatives have tangible returns that may be below the other investment options but are justifiable uses of capital because they have a meaningful positive social or environmental impact.

We are investors first and foremost. Our paramount responsibility is to protect and grow the wealth of our clients. Because the stock market is a complex adaptive system, investment teams must evolve in order to understand opportunities and translate them into excess returns. We believe impact externalities, both positive and negative, will be internalized over the long term. Sustainable Research allows us to gather data that is more useful than that from traditional ESG screens. As a result, we can capture insights from company management and observe trends that were previously hidden.

Our Sustainability Research framework and SR Tailwinds benefit our clients through our differentiated insights. An estimate of the value of impact externalities in the valuation process allows us to assess investment opportunities more holistically. And as these metrics become more mainstream, companies will have an incentive to create value and capitalize on opportunities that have a positive impact on the environment and society.

Wrap-up

If you’ve got any thoughts, questions, or feedback, please drop me a line - I would love to chat! You can find me on twitter at @kevg1412 or my email at kevin@12mv2.com.

If you're a fan of business or technology in general, please check out some of my other projects!

Speedwell Research — Comprehensive research on great public companies including Copart, Constellation Software, Floor & Decor, Meta, RH, interesting new frameworks like the Consumer’s Hierarchy of Preferences (Part 1, Part 2, Part 3), and much more.

Cloud Valley — Easy to read, in-depth biographies that explore the defining moments, investments, and life decisions of investing, business, and tech legends like Dan Loeb, Bob Iger, Steve Jurvetson, and Cyan Banister.

DJY Research — Comprehensive research on publicly-traded Asian companies like Alibaba, Tencent, Nintendo, Sea Limited (FREE SAMPLE), Coupang (FREE SAMPLE), and more.

Compilations — “A national treasure — for every country.”

Memos — A selection of some of my favorite investor memos.

Bookshelves — Your favorite investors’/operators’ favorite books.