Letter #162: John Zito (2011)

Apollo Deputy CIO of Credit and Partner | Zito Discusses Trading in Tepco's Credit-Default Swaps

Hi there! Welcome to A Letter a Day. If you want to know more about this newsletter, see "The Archive.” At a high level, you can expect to receive a memo/essay or speech/presentation transcript from an investor, founder, or entrepreneur (IFO) each edition. More here. If you find yourself interested in any of these IFOs and wanting to learn more, shoot me a DM or email and I’m happy to point you to more or similar resources.

If you like this piece, please consider tapping the ❤️ above or subscribing below! It helps me understand which types of letters you like best and helps me choose which ones to share in the future. Thank you!

Today’s letter is the transcript of an interview with John Zito. This is a particularly interesting letter because rather than simply discussing high level investing philosophy and process, John actually walks through his thought process around two specific trades: TEPCO CDS after the Fukushima nuclear accident and a Q-Cells rally on the back of speculation on alternative sources of energy. In it, he compares debt vs equity investors and markets and touches on market conditions, his process, liquidity, orphaned assets, and converts and busted converts.

John Zito is a Partner and Deputy CIO of Credit at Apollo, overseeing the firm’s global Credit business and team (which makes up ~$450bn of Apollo’s total ~$630bn AUM). John is also a member of the Firm’s Leadership Team. Apollo’s platform spans the full financing universe across public and private markets, including corporate credit, direct lending, asset-backed finance and more. Prior to joining Apollo in 2012, John served as a Managing Director and Portfolio Manager at Brencourt Advisors and previously spent five years as a Portfolio Manager at Veritas Fund Group.

I hope you enjoy this interview as much as I do!

[Transcript and any errors are mine.]

Related Resources

Apollo

Investors

Portfolio Companies

Yahoo!: A Decade of Activism - Yahoo! Activists Compilation (187pgs)

Transcript

Host: One company still on the decline is at the epicenter of Japan's nuclear crisis. I'm talking about Tokyo Electric Power. They, of course, have reacted quite strongly, have lost about $24bn in market value. Well, here as part of our dark side series, we're talking to a credit specialist--a credit market specialist. His name is John Zito, he's the portfolio manager for credit opportunities at Brencourt Advisors, an employee-owned hedge fund sponsor. And he joins us now with his perspective, or sort of the credit market's perspective, on events in Japan. I was just mentioning that TEPCO, Tokyo Electric Power, they operate the Fukushima plant, their stock has just been completely obliterated. But there is a lot going on, in sort of the credit market side of things. CDS spreads have blown out quite dramatically over the just the last few days.

John Zito: Yeah, I would say, over the weekend, a big trade that a lot of credit managers were talking about was buying the protection of the CDS of TEPCO. So, it was trading around 120-150bps off the curve, if you looked at it on Bloomberg over the weekend.

As part of our process, we always look at all the key players in any sort of reaction like this. It's a tragedy, but obviously, you have to do your work and see where all the tail risks are. In this case, if you look at TEPCO, 38% of their production actually comes from nuclear. So if you look behind the curtain, they're actually have about $8bn of debt. And they only do $1bn of EBITDA. The uncertainty around the costs, there's a ton of uncertainty around what the cleanup costs could be, what the ramifications are going forward. And as credit managers, I think the big difference between equity and credit managers are the credit managers look at the balance sheet, they look at the risks, they look at the uncertainty, and then they price that uncertainty. So a lot of credit managers were doing the work over the weekend, and you could actually buy protection at 150bps off on Sunday night or Monday morning, and subsequently it's gone from 150bps off to 400 off.

Host: Now the interesting thing, unlike what we see in the equity markets, really, for a stock like a Tokyo Electric, there's enough liquidity there for anyone to take either side of the trade. But in the credit default swap market, that's not always the case.

John Zito: Yeah. One thing--in this case, actually, the triggers got--on TEPCO, the equity, you actually--it didn't ever trade. Because it opened, traded down 5%, hit a trigger, it went down 5%, it went down again. But to your point, on the CDS market, only a little bit of volume was going through. That's why it moved so quickly. But there were trades going on in the morning prior to the second or third explosion there. But there's still--it's much more liquid than it was, let's say 10 years ago. That markets gotten more--

Host: John, I want to talk to you about another trade that you and I discussed about solar cells. We talked about this yesterday, actually, on this show, that a lot of solar companies are doing quite well, at least on the stock side. I want to talk to you about what is happening on the debt side of that trade. We're going to have more in just a moment…

John, we were talking a little bit about TEPCO, because that's a company that is making a lot of headlines today with the Fukushima plant. But let's talk about solar cells. This is actually an industry where solar companies have actually rallied as people speculate on alternative sources of energy. Tell me how you're playing that trade.

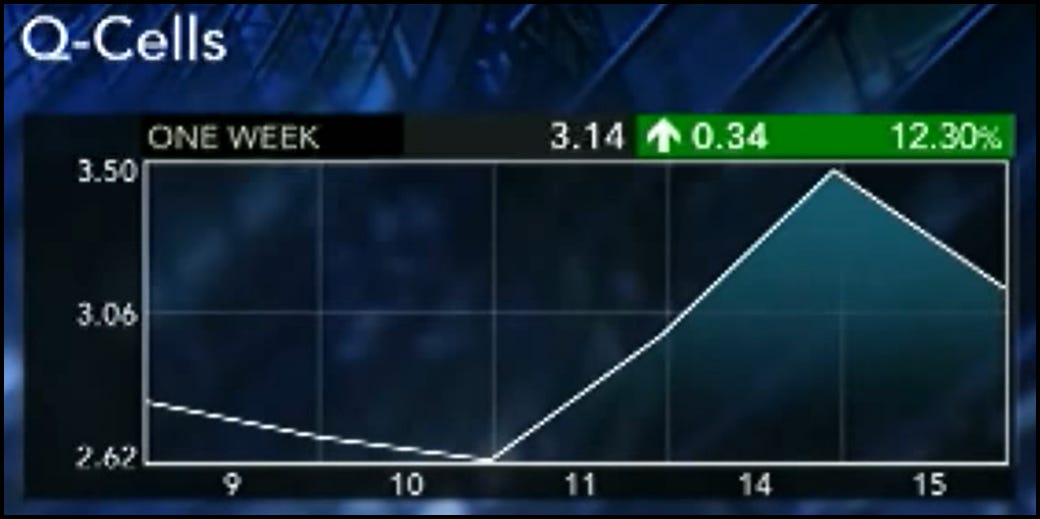

John Zito: As a multi-strategy fund, we can look at debt, equity, loans--so any part of the capital structure. So we've tried to find inefficiencies within between debt and the equity markets, and what you've seen since Friday of last year, if you can pull up the chart…

… you'll see that the Q-Cell’s equity, which is the biggest solar cell manufacturer in the world, the stock has gone from--is up 25%, over the last three days. And if you look--Oh, at some point, it was up 40%. While that has been going on, the actual debt is actually down over the last three days. So you can still buy the debt at a 15% Yield to Maturity over three years, and not take the fundamental risk longer term, i.e.; subsidies or any--with all the--you'll hear all the bears talk about all the bearish scenarios for solar and how it doesn't work versus grid parity.

Host: Now, do you think it's because the credit market knows something the equity market doesn't or in this case, is the equity market is getting ahead of itself?

John Zito: Yeah, I mean, Brencourt specializes in kind of orphaned assets. So in this case, this is a busted convert, which means there's no actual equity optionality to the convert because solar’s been hit so hard over the last couple years. So traditional high yield managers can't buy it, because it's a convert. But traditional convert managers can't buy it because there's no equity optionality to it anymore. So it just kind of sits in this weird spot. So we do the--

Host: Well John, you just said a whole lot of things that a lot of us don't understand. But that's why we're doing this series. So let's just start with, when you talk about it being a convert and the optionality really not being worth very much, let's--explain that, break that down in simple terms.

John Zito: Sure. In Q-Cell's case, the strike price on the call option within the convert is $85, and the stock trades at--three--

Host: A convertible bond meaning--which is an unusual structure, sort of a hybrid bond that allows for you to convert it to equity once the stock gets above a certain level, in this case, because Q-Cell’s stock dropped so much.

John Zito: Because it's so far out of the money, the option has no value. So it really behaves more like a high yield bond. But high yield bond managers, because of their mandate, can't own it. So it creates the opportunity. And when--if you can pull up the difference between the equity market value and the debt market value, you'll see that there's a much bigger margin of safety. And it creates a much more low volatility risk return profile to the position, and enables us to play a theme which in this case is solar, in a much less risky way with a higher probability of making a return.

Host: Well, at the risk of oversimplifying, let me just say this: So this is one of those situations where instead of buying the stock to get exposure to this company, going in and buying this convertible bond, you get a high yield that's sort of mispriced because it only has a limited number of potential buyers. But this is an interesting way to sort of look at what is happening in events in Japan and how investors in your market are taking advantage of opportunities.

John Zito: Yeah, it's important. I mean, what you see also is that the equity markets look at growth. So solar could be a much bigger market down the road. So they give them the benefit of the doubt. Credit managers are much more focused on balance sheet, on cash flow, and the downside. They're much more risk averse. Whereas equity managers are much more momentum driven, and you'll see much more top line growth being the key aspect of any sort of stock story. So that--we try to arbitrage those two opportunities in terms of value creation.

Host: All right, John, I so appreciate you coming. We got to have you back so you can explain some more of this stuff, because it's a new language for many people. That was John Zito, at Brencourt Advisors.

If you got this far and you liked this piece, please consider tapping the ❤️ above or sharing this letter! It helps me understand which types of letters you like best and helps me choose which ones to share in the future. Thank you!

Wrap-up

If you’ve got any thoughts, questions, or feedback, please drop me a line - I would love to chat! You can find me on twitter at @kevg1412 or my email at kevin@12mv2.com.

If you're a fan of business or technology in general, please check out some of my other projects!

Speedwell Research — Comprehensive research on great public companies including Constellation Software, Floor & Decor, Meta, new frameworks like the Consumer’s Hierarchy of Preferences (Part 1, Part 2, Part 3), and much more.

Cloud Valley — Easy to read, in-depth biographies that explore the defining moments, investments, and life decisions of investing, business, and tech legends like Dan Loeb, Bob Iger, Steve Jurvetson, and Cyan Banister.

DJY Research — Comprehensive research on publicly-traded Asian companies like Alibaba, Tencent, Nintendo, Sea Limited (FREE), and more.

Compilations — “A national treasure — for every country.”

Memos — A selection of some of my favorite investor memos.

Bookshelves — Your favorite investors’/operators’ favorite books.