Letter #190: Lo Ying Shek (2003)

Great Eagle Holdings Founder, Chairman, and Managing Director | 2002 Chairman's Statement

Hi there! Welcome to A Letter a Day. If you want to know more about this newsletter, see "The Archive.” At a high level, you can expect to receive a memo/essay or speech/presentation transcript from an investor, founder, or entrepreneur (IFO) each edition. More here. If you find yourself interested in any of these IFOs and wanting to learn more, shoot me a DM or email and I’m happy to point you to more or similar resources.

If you like this piece, please consider tapping the ❤️ above or subscribing below! It helps me understand which types of letters you like best and helps me choose which ones to share in the future. Thank you!

Today’s letter is Lo Ying Shek’s 2002 Great Eagle Holdings Chairman’s Statement. This was the last letter he wrote shareholders before naming his son Lo Ka Shui Deputy Chairman and passing along letter writing responsibilities to. In this letter, Lo gives an update on rental properties in Hong Kong and the US, hotels and furnished apartments in Hong Kong and internationally, properties under development, trading, and property management. He then goes over the group’s financials, starting with debt, the finance cost, then liquidity and debt maturity profile, pledge of assets, and commitments and contingent liabilities. After covering finances, he shares his outlook for the future before ending with a few notes on staff, dividends, the closure of transfer books, and a thank you to staff members and directors.

Lo Ying Shek was the Founder, Chairman, and Managing Director of Great Eagle Holdings. Born in China, Lo moved to Thailand along with his father to work in the textile industry. After getting married, he moved to Hong Kong to work in the cloth and dye trading business. 25 years after moving to Hong Kong, in 1963, he started Great Eagle Company with his wife (the name Great Eagle Company was derived from Lo and his wife’s names). Great Eagle went public on the Hong Kong Stock Exchange in 1972, and in 1990, went through a reorganization and was renamed Great Eagle Holdings. Over the decades, he led Great Eagle into becoming one of the largest real estate developers in Hong Kong, with a strong presence in the development, investment, and management of high-quality office space, shopping malls, residential, and hotel properties across Hong Kong, Mainland China, Japan, North America, Australia, and Europe. At one point, they directly controlled ten Hong Kong public companies.

I hope you enjoy this letter as much as I do!

Related Resources

Real Estate

Asia

Letter

During 2002, our hotel business in Hong Kong performed ahead of expectations with improved yields and better income. Otherwise the Group’s businesses, both local and overseas, continued to operate under difficult market conditions. Generally lower interest rates however have helped cushion the decline in our overall income.

Operations Review

1. Rental Properties

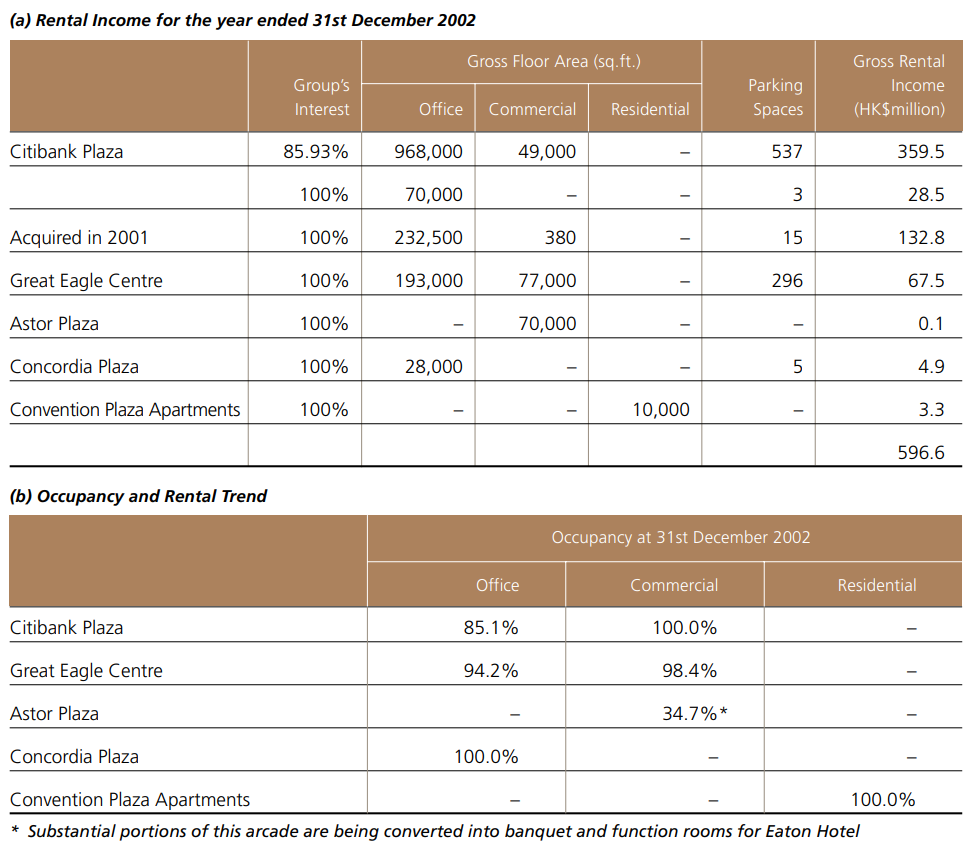

Hong Kong Rental Properties

The Grade-A office market in Hong Kong weakened further during 2002. Despite a low level of new supply, the continued downsizing of corporations, especially in the financial sector, released a substantial amount of redundant spaces, pushing overall vacancy rates into double-digits. Effective rent rates also went down fairly significantly as a result.

Net rental income from our Hong Kong rental portfolio decreased by a modest 7.1% from $597.1 million in 2001 to $554.5 million in 2002. The portfolio’s income benefited by the full-year accounting of income from the office space purchased from Citibank in mid-2001.

U.S. Rental Properties

The continued softening of the California office markets resulted in lower occupancy and lower rental rates. As a result revenues in 2002 were 18.4% less than in 2001. The properties in the San Francisco Bay Area were particularly hurt by the decline of the dot.com industry, which had resulted in the bankruptcy of a number of tenants. The property at 888 West Sixth Street Los Angeles, which became 100%-owned in June 2002, performed well with improved occupancy of 94%. Furthermore, recent rental activities at all our properties show encouraging signs that rental rates may have bottomed already. We expect occupancy to improve in the coming year.

2. Hotels and Furnished Apartments

The impact of the September 11 incident and the global economy downturn continued to weigh down the industry’s performance overall, especially from the long haul leisure markets of the USA and Europe. Business travel also saw little growth momentum, resulting in continued softness in room rates for the overseas hotels.

The Hong Kong hotel market performed relatively better due to increased tourist arrivals from Mainland China, which filled up the lower end market and in turn benefited the high end hotels. Further relaxation in travel restrictions and increasing affluence on the Mainland are likely to have major positive impact in the coming years.

In February 2003, the Group’s hotel management division Great Eagle Hotels International was re-branded as Langham Hotels International, after the prominent Langham Hotel owned by the Group in West End London. This new brand name, with its prestigious quality image, will set the benchmark for the Group’s future global hotel expansion.

Hong Kong Operations

Great Eagle Hotel, Hong Kong

Underpinned by the strength in convention business, the hotel performed reasonably well in 2002 with an increased occupancy of 83% (2001: 79%), while maintaining average room rate levels at HK$823 (2001: HK$829). Net operating income for 2002 grew 13.4% over the previous year.

The hotel will be renamed Langham Hotel in October 2003.

Eaton Hotel, Hong Kong

The growth in visitors from the China market and the perception of Hong Kong as a safe destination strengthened the leisure market segment in 2002. For the year the hotel maintained a high occupancy at 83.5% (2001: 84.6%) and improved the average room rate to HK$443 (2001: $426).

Net operating income of the Hotel jumped 40.3% in 2002 mainly due to a 22% increase in food and beverage revenue, brought about by a strategic decision to focus on banqueting services. Additional portions of Astor Plaza underneath the Hotel have been or are being converted into banqueting facilities and function to further enhance its local banqueting, meeting and conference business in 2003.

Eaton House Furnished Apartment, Hong Kong

Overall performance weakened as a result of a substantial reduction in corporate demand and increased competition from hotels and new supply of serviced apartments. Eaton House registered an average occupancy of 69% in the year 2002 (2001: 75%).

International Operations

The Langham Hilton, London

Although trading was much influenced by post September 11 activities, which lasted into the first quarter of 2002, and a slow summer, The Langham’s performance improved in the last quarter of the year with increased international travel and residential conference business. However, London remains soft on rates overall due to expense tightening by corporations and uncertainty arising from the possibility of war in Iraq.

For the year 2002, the hotel achieved an average occupancy of 69% and an average room rate of £151 as compared to 68% and £159 in 2001. The performance was in line with the market

Delta Chelsea Hotel, Toronto

As fears generated from the terrorist attack of September 11 started to recede, the struggling economy, especially in the United States started to emerge as the major deterrent to travel. International business, corporate travel, overseas tours and leisure business slowed down considerably in the city and those few citywide conventions planned softened from original expectations.

Despite those difficulties, for the year 2002, the hotel achieved an average occupancy of 66% and maintained an average room rate of C$141 as compared to 73% and C$139 in 2001.

Sheraton Towers Southgate Hotel, Melbourne

Whilst the Australian domestic economy was able to continue its growth during 2002, the world economic situation continued to impact on consumer and business confidence. The increasing security threats and lack of citywide meetings and conventions has weakened the long haul market and corporate travel. The Melbourne 5- star hotel market reflected this with room yields decreasing by up to 11%.

Despite this, for the year 2002, the hotel achieved an average occupancy of 69% and an average room rate of A$217 as compared to 73% and A$223 in 2001 for an overall modest yield improvement on the market trend.

Hotel Le Meridien, London

Year 2002 was another difficult year for the US lodging industry, and for Boston in particular, as revenues declined for the second year in a row. Although the year began with significant year-over-year declines in occupancy, many hotels were able to stimulate demand by cutting rates sharply.

For the year 2002, the hotel achieved an average occupancy of 70% and an average room rate of US$200 as compared to 65% and US$236 in 2001. Business traffic remains soft while the US economy looks for new directions. Completion of a new Convention and Exhibition Centre and the final stage of the ‘Big Dig’, the largest tunnel and highway project in US history which will dramatically improve congestion and mobility in the city are future positive steps for this destination.

Sheraton Auckland Hotel and Towers, Auckland

Although meeting and conference business market segments were depressed throughout the city, there was revenue growth in the Leisure market segments partly led by the early trials for the America’s Cup and the successful results from the Tourist Board’s recent campaigns. Continuing competitiveness within the market from serviced apartments ensured room rates remained suppressed in the year despite a strengthening in overall arrivals.

For the year 2002, the hotel achieved an average occupancy of 65% and an average room rate of NZ$144 as compared to 68% and NZ$142 in 2001.

3. Properties Under Development

Mongkok Project

Construction of the superstructure and the basements commenced at the start of 2002 and made significant progress during the year. By year-end the building structures had reached the following levels:

Topping out of the three building structures will take place in mid2003 whilst construction of the building envelopes and internal fitting out will continue through 2004. Final design of the architectural features of the shopping centre, curtain walling of the office tower and the interior finishes of the hotel have been largely completed. We strongly believe that total commitment to quality will be key to the eventual success of the project. State-of-the-art building features have been incorporated into the design of the Grade-A office tower and the luxury hotel. We have also brought in internationally renowned shopping centre designers Jerde & Associates to work alongside project architects Wong & Ouyang in creating innovative architectural features for the shopping centre, which will offer an unprecedented and exciting experience to shoppers in Hong Kong. Issuance of the occupation permit for the entire complex is targeted for the end of first quarter 2004. The hotel and the shopping centre components of this massive complex are expected to open for business in the third and fourth quarters of 2004 respectively.

Preparation for the marketing and leasing of the shopping centre, under the advice of major international shopping centre consultants and a top worldwide advertising agency, is at an advanced stage. A major cinema chain has signed a preliminary agreement to lease and operate the 6-screen cineplex. Formal launch of the leasing campaign is scheduled for the third quarter of 2003.

The hotel at the Mongkok Project, with a total of 719 room bays (some rooms having been converted into spa, gymnasium and club facilities), has been upgraded to a 5-star hotel in justification of its generous room sizes, its quality design and finishes and its strategic MTR location. Named the Langham Place Hotel, it has been introduced to the international hotel industry in early March 2003.

The total expenditure incurred in relation to the project, including interest capitalised, amounted to HK$7,809 million as of year-end 2002 (2001: HK$6,700 million). The HK$5,100 million construction loan was refinanced in December 2002 at a more favourable interest spread. The extension of loan maturity to December 2008 will also allow more flexibility in the leasing of the property. The undrawn loan commitment of HK$3,670 million as of 31st December 2002 should be sufficient to fund the project to completion.

4. Trading

Hong Kong’s sluggish property market continued to affect the performance of the construction materials trading arm Toptech Co. Ltd. in 2002. Total revenue for 2002 amounted to HK$164 million, a drop of 7% from 2001. However, effective cost control resulted in a moderate increase in gross profit contribution from the business.

5. Property Management

Competition in the property management industry remained keen in 2002, as property owners demanded for lower management charges and manager’s remuneration. While we managed to maintain a stable portfolio of buildings under management, there was a drop of 1.4% in income from HK$17.9 million in 2001 to HK$17.7 million as a result of reduction in manager’s remuneration upon renewal of contracts.

Top line revenue of our engineering division remained under pressure during 2002 because of the slow economy. However as a consequence of improved productivity and cost control, the division showed a 36% improvement in contribution from HK$6.6 million in 2001 to HK$9.0 million in 2002.

Financial Review

Debt

Consolidated Net Attributable Debt as of 31st December 2002 was HK$11,955 million, an increase of HK$879 million over that at yearend 2001. The increased borrowings were mainly related to Mongkok project expenditures.

Consolidated Net Asset Value, based on professional valuation of the Group’s investment properties and other assets at cost, amounted to HK$14,604 million as of 31st December 2002, a decrease of HK$519 million from that of yearend 2001. The resulting gearing ratio at 31st December 2002 was 82%.

As at 31st December 2002, we had outstanding interest rate swaps with total notional principal of HK$2,420 million, representing 26% of our HK$-denominated debts. With HK$ interest rates trending lower throughout 2002, we kept 74% of our HK$ borrowings on floating-rate basis. As a result we achieved further significant savings in interest expenses.

Our foreign currency debts, taken out to finance our overseas hotels and U.S. office properties, amounted to the equivalent of HK$3,801 million as of 31st December 2002. All these foreign currency borrowings are fully hedged by the value of the underlying properties. Of this, the equivalent of HK$1,059 million, or 28% of our foreign currency debts, was on fixed-rate basis.

Finance Cost

The net finance cost incurred during 2002 was HK$326.6 million, as compared to the HK$427.3 million charged in 2001. Substantially lower interest rates had more than offset the effects of the higher debt level. In addition, HK$246.5 million of finance cost relating to the Mongkok Project was capitalized, only marginally higher than that of HK$244.1 million for 2001. Lower interest rates largely offset the effect of incremental project expenditures.

Overall interest cover for 2002 was 2.08 times, improved from that of 1.71 times for 2001.

Liquidity and Debt Maturity Profile

As of 31st December 2002, our cash, bank deposits and committed but undrawn loan facilities amounted to a total of HK$4,470 million. The majority of our loan facilities is medium-term in nature and is secured by properties with comfortable value to loan coverage. The following is a profile of the maturity of outstanding debts as of 31st December 2002.

Pledge of Assets

At 31st December 2002, the Group’s properties with a total carrying value of approximately HK$28,125 million (2001: HK$27,773 million) together with assignments of sales proceeds, insurance proceeds, rental income, revenues and all other income generated from the relevant properties and deposits of approximately HK$4.6 million (2001: HK$95.4 million) were mortgaged or pledged to secure credit facilities granted to the Group.

Commitments and Contingent Liabilities

The Group

At 31st December 2002, the Group had commitments and contingent liabilities not provided for in these financial statements, as follows:

(a) estimated expenditure in respect of property under development amounting to approximately HK$2,947 million (2001: HK$3,706.7 million) of which approximately HK$2,456.8 million (2001: HK$3,255.3 million) were contracted for;

(b) authorised capital expenditure amounting to approximately HK$74.4 million (2001: HK$43.5 million) of which approximately HK$13.3 million (2001: HK$18.8 million) were contracted for; and

(c) commitments under foreign exchange future contracts to sell approximately HK$154.3 million (2001: HK$143.9 million) at fixed exchange rates.

The Company

At 31st December 2002, the Company had issued corporate guarantees to certain banks in respect of credit facilities drawn by its subsidiaries amounting to approximately HK$9,915 million (2001: HK$9,248 million).

Other than set out above, the Group and the Company did not have any significant commitments and contingent liabilities at 31st December 2002.

Outlook

Our Hong Kong hotels should be the most promising among our various business segments in terms of performance in 2003. The HKSAR Government’s strong commitment to promoting a larger flow of tourists from Mainland China will benefit the hotel industry generally in Hong Kong. With a sustainable high level of occupancy, there should be room for modest upward adjustments in room rates. Our overseas hotels should perform better in 2003 than 2002, although it will still depend on how events in the Middle East would unfold.

The present softness in the Hong Kong office market will probably continue through 2003, as new buildings to be completed in the second half would compete more aggressively for tenants by way of pricing. The cost of retaining existing tenants will exert downward pressure on the income from our Hong Kong office properties for the current year. However with rents having decreased to fairly low levels, there has been a notable increase in the number of enquiries from and movement of tenants currently at peripheral locations back to Hongkong Island business districts. This should have a medium-term stabilizing effect on occupancy and rent rates for our Central and Wanchai properties.

We have made significant progress in the construction of the Mongkok project in the past year. At the same time innovative value-added features are being incorporated into the design to turn this landmark development into a one-of-a-kind complex worthy of its very prime location. Initial feedback from our pre-marketing efforts has been most encouraging. We are confident of the positive response to our marketing campaigns for the shopping centre and the hotel when they are officially launched later this year.

Staff

The total number of employees in the Group was 2,689 as of 31st December 2002. Salaries of employees are maintained at competitive levels while bonuses are granted on a discretionary basis. Other employee benefits include educational allowance, insurance, medical scheme and provident fund schemes. Senior employees (including executive directors) are entitled to participate in Great Eagle Holdings Limited Share Option Scheme (formerly Executive Share Option Scheme). In order to improve employees’ morale and sense of teamwork, some measures were considered by the Group’s senior management in the 2002 year end to enhance employee benefits and training as well as to enhance employee relations through internal communications and recreation activities.

Dividends

The Board has resolved to recommend to Shareholders at the forthcoming 2003 Annual General Meeting (the “2003 AGM”) the payment of a final dividend of HK10 cents per share for the year ended 31st December 2002 (2001: HK14 cents per share), to be satisfied by way of a scrip dividend with a cash option, to Shareholders whose names appear on the Register of Members on 14th May 2003. Together with the interim dividend of HK5 cents per share paid on 24th October 2002, on the assumption that every Shareholder elects to receive all final dividend in cash, the total dividend for the full year will be HK15 cents per share (2001: HK21 cents per share), amounting to not less than HK$87,446,723 (2001: HK$121,205,158).

Subject to the approval of Shareholders at the 2003 AGM and the Listing Committee of The Stock Exchange of Hong Kong Limited granting listing of and permission to deal in the new shares to be allotted and issued pursuant to the proposed distribution of a scrip dividend mentioned herein, each Shareholder will be allotted fullypaid shares having an aggregate market value equal to the total amount which such Shareholder could elect to receive in cash and will be given the option to elect to receive payment partly or wholly in cash instead of the allotment of shares. Dividend warrants and share certificates in respect of the proposed dividend are expected to be despatched to Shareholders on or about 16th June 2003. Full details of the scrip dividend will be set out in a letter to be sent to Shareholders together with a form of election for cash soon after the 2003 AGM.

Closure of Transfer Books

The Register of Members of the Company will be closed from Tuesday, 6th May 2003 to Wednesday, 14th May 2003, both days inclusive, during which period no share transfers will be effected.

For those Shareholders who are not already on the Register of Members, in order to qualify for the final dividend, all share certificates accompanied by the duly completed transfers must be lodged with the Hong Kong Branch Registrars of the Company, Computershare Hong Kong Investor Services Limited (formerly Central Registration Hong Kong Limited) of 17th Floor, Hopewell Centre, 183 Queen’s Road East, Wanchai, Hong Kong for registration not later than 4:00 p.m. on Monday, 5th May 2003.

Finally, I would like to take this opportunity to express my appreciation and thanks to all staff members for their dedication and hard work and to address my sincere gratitude to my fellow Directors for their support and guidance in the past year.

Lo Ying Shek

Chairman

Hong Kong, 11th March 2003

If you got this far and you liked this piece, please consider tapping the ❤️ above or sharing this letter! It helps me understand which types of letters you like best and helps me choose which ones to share in the future. Thank you!

Wrap-up

If you’ve got any thoughts, questions, or feedback, please drop me a line - I would love to chat! You can find me on twitter at @kevg1412 or my email at kevin@12mv2.com.

If you're a fan of business or technology in general, please check out some of my other projects!

Speedwell Research — Comprehensive research on great public companies including Constellation Software, Floor & Decor, Meta, RH, interesting new frameworks like the Consumer’s Hierarchy of Preferences (Part 1, Part 2, Part 3), and much more.

Cloud Valley — Easy to read, in-depth biographies that explore the defining moments, investments, and life decisions of investing, business, and tech legends like Dan Loeb, Bob Iger, Steve Jurvetson, and Cyan Banister.

DJY Research — Comprehensive research on publicly-traded Asian companies like Alibaba, Tencent, Nintendo, Sea Limited (FREE SAMPLE), Coupang (FREE SAMPLE), and more.

Compilations — “A national treasure — for every country.”

Memos — A selection of some of my favorite investor memos.

Bookshelves — Your favorite investors’/operators’ favorite books.