Letter #245: Peter Thiel and Josh Wolfe (2019)

Founder of PayPal, Palantir & Founders Fund and Founder of Lux Capital | Harnessing and Securing American Innovation: How Venture Capital Impacts Defense

Hi there! Welcome to A Letter a Day. If you want to know more about this newsletter, see "The Archive.” At a high level, you can expect to receive a memo/essay or speech/presentation transcript from an investor, founder, or entrepreneur (IFO) each edition. More here. If you find yourself interested in any of these IFOs and wanting to learn more, shoot me a DM or email and I’m happy to point you to more or similar resources.

If you like this piece, please consider tapping the ❤️ above or subscribing below! It helps me understand which types of letters you like best and helps me choose which ones to share in the future. Thank you!

Peter Thiel is a Founder of Thiel Capital, PayPal, Palantir, Founders Fund, Clarium Capital, Valar Ventures, Mithril Capital, the Thiel Foundation, and the Thiel Fellowship. He was also the first outside investor in Facebook. Peter started his career as a clerk for Judge James Larry Edmondson of the US Court of Appeals for the 11th Circuit before joining Sullivan and Cromwell as a securities lawyer. He left after 7 months. He then joined Credit Suisse as a derivatives trader in currency options and concurrently worked as a speechwriter for former US Secretary of Education William Bennet. (Full compilation here.)

Josh Wolfe is a Founder of Lux Capital and a Trustee at the Santa Fe Institute. As a high schooler, he did cutting edge AIDS research before studying business and going into investment banking. But after just one year in banking, Josh teamed up with Peter Hebert and convinced Bill Conway (Founder of Carlyle) to give them a ~$10mn sleeve to invest into nanotech (it was the height of the dotcom boom and everyone was investing in everything internet). Another early LP was Stan Druckenmiller. When Bill asked Josh and Peter how they would beat Sequoia and Kleiner, they went and built out an entire research arm (Lux Research, now a standalone company, which produced 500pg+ nanotech reports that attracted early customers such as Vinod Khosla), a public policy arm (that engaged Nobel prize winners and key regulators), and a media arm (the Forbes/Wolfe Emerging Tech Report - I’ve compiled the editions I had in my Josh Wolfe compilation).

Today’s letter is the transcript of Peter’s and Josh’s responses on a panel at the Reagan National Defense Forum titled Harnessing and Securing American Innovation: How Venture Capital Impacts Defense. On this panel, Peter and Josh discuss venture opportunities in defense, the shift in global R&D spend, liquidity for defense investments, defense spending, M&A in the defense industry, and the effects of government regulation limiting profits.

I hope you enjoy this panel as much as I did!

[Transcript and any errors are mine.]

Related Resources

PayPal

Palantir

Founders Fund

Cyan Banister Biography (Cyan: The enlightenment of an iconoclast)

Meta Podcast (2 hours) [Free]

Meta Deep Dive (Full report: 166 pages)

Meta Business History (~18 pages)

Lux Capital

Santa Fe Institute

Letters

Compilations

Indexes (Interactive Compilation)

Transcript

On Venture Opportunities in Defense

Host: Peter, you could probably count on one hand how many companies, startups, are out there in the country right now that are focused on national security in some form or fashion, and that have reached so-called unicorn status, meaning a billion-dollar valuation or greater. I believe you've funded all or nearly all of those companies. How do you think about this?

Peter Thiel: Well, by my count, the number is two. If we look at companies started since the end of the Cold War, last 30 years, 1980 to 2019, there's SpaceX and Palantir. And I was co-founder of Palantir and I was the first outside investor in SpaceX. So I've been heavily involved in both of those. And I think there's always sort of like a glass half full, glass half empty version. The glass half full version is that--I think innovation will get driven by--a lot of innovation gets driven by smaller companies that get started and that scale over time. And so this is absolutely critical, when not that many people are doing it. If you're one of the few who does it, there's a lot of opportunity. And then at the same time, we have to acknowledge that in the aftermath of the Cold War, there were sort of ways in which the military sort of contracted into this sort of posture where all the funding went to the major primes, and it became much harder for this sort of small to mid sized entrepreneurial system to build. And I think as a venture capitalist, you don't want to invest in tiny consulting companies that always stay tiny, and where there's some idiosyncratic use and it sort of goes into a cul de sac that's a broom closet in the Pentagon or something like this. You want to do things that scale, that get bigger over time. And this has sort of been--and I think there's definitely a lot of--there are a number of attempts have been made in recent years in the US military to try to correct for this sort of procurement process, but I still think we have a ways to go.

Host: Josh, you're invested in a number of companies as well that are focused on national security and defense. How do you see it as an investor? And are there those opportunities beginning to emerge now to grow and to scale, especially at a time where so many other VCs are focusing on companies that are consumer facing or enterprise facing given the fact that those do tend to be growth areas.

Josh Wolfe: There definitively are opportunities. And I want to echo something that [the sec def] said, which was that it's about the people. And so if you start even with the motto here of peace through strength--strength in part comes from technological dominance, and technological dominance in part comes from brilliant engineers that are inventing the most cutting edge technologies to outcompete peer competitors. And so if you spend time with somebody like Palmer Luckey at Anduril that you may have seen walking around the halls, or Trae or Brian--these are authentic engineers that are obsessed with technology, that are constantly thinking about what does the warfighter need? Where's the white space? What's the gap? What is China developing? What is Russia developing? And how can we equip them with the most cutting-edge technologies that are out there? And so if you go with the cliched view that the best way to predict the future is to invent it, the people that are inventing the future are the engineers that are really toiling and doing some of the most cutting edge work. Many of those people are inspired by science fiction. They are literally going back 20 years into the annals of comic books and sci-fi movies and saying, It would be amazing if we had that. And by the way, when you speak to top military brass, they say the same thing. T2--Tony Thomas--said when he was in Afghanistan, he wanted the Minority Report-like gloves to be able to navigate through information space. And I think when you talk to all top warfighters, they're saying, We want the stuff that we see in the movies. Well, the people that are inventing that are these young entrepreneurs and these young cutting-edge engineers. And I agree 100% with what Peter said--I think we have a totally flawed system where you have people that feel in government like they are checking the box by allocating a little bit of capital to many projects. And they're doing the country, and these companies, frankly, a massive disservice. We don't do that. As venture capitalists, we don't put $250k or $500k into 100 companies--you really try to double down on who are the best teams developing the most cutting-edge technology. And you really put a fewer number of eggs in a fewer number of baskets. So I think if there's one thing that we could change, it would be really to concentrate bets into the absolute best. To give not only these companies an advantage, but to give the country an advantage.

Host: So you just touched on something. I want to just flesh this out a little bit more because when we were getting ready for this panel, one of the points that was raised was this idea that maybe folks that are involved in military work or in the defense community don't fully understand or fully know what it means to--what venture capital investment means. So just my quick elevator pitch, a little background here, that a venture capitalist is an investor who provides capital to firms that exhibit high growth potential, as we just talked about, in exchange for an equity stake. VCs target firms that are at the stage where they are looking to commercialize their idea. High risk, high reward. You can see high rates of failure due to the uncertainty that is involved with new and unproven companies. I read one stat that something like 70% of startup companies tend to fail?

Josh Wolfe: It might even be higher. I mean if you think about our world, is much about frequency versus magnitude. In military, you of course can take significant calculated risks, but the consequence of failure is much greater. 90% of the things that we fund could fail--if the 10% that succeeds succeed in such a magnitude that it makes up for all the losers. And so we are willing to take--and our investors that give us money--pension funds and endowments and wealthy families--expect that exact risk-taking. They expect us to invest in things that are going to create multi-billion dollar future businesses. And they're totally okay if the long tail of other stuff that we fund ends up being absolutely worthless.

Peter Thiel: And then the corollary to that that's very important to draw out out is, if you can't create a business worth a billion dollars or more, the venture capital model does not work that well. So if you start a company and it's worth $30mn, $100mn, that can be quite successful for the person starting a company--for a venture fund, that actually--if that's the best we did in any of our companies, we would be out of business. So you need to get some that can really break through at scale. And so we're not investing in hot dog stands--which could be a great business, but is not going to scale. We have to--we invest in companies that start small but have the potential to grow and scale to sort of a world class scale.

Host: Which begs the question, I think, because you just mentioned Palantir and Space X. Certainly SpaceX is changing the way that rockets are flown. Has it created, or have these companies created, a template for other startups to follow within the space?

Peter Thiel: Well there's certainly proof that it can be done. It, in both cases, took a wickedly long time. Probably close to a decade to start getting significant contracts from the US Military. And in some ways, they were not conventionally venture fundable. I personally funded Palantir, Elon personally funded SpaceX. We got outside capital maybe six years into both businesses. And so if you have something where you have a six year gap and can only get funded by someone who's putting in tens of millions of dollars as a sort of slightly quixotic project, that's a tricky template to repeat. I think there definitely are lessons one can learn from Palantir and SpaceX. We made a lot of mistakes. There may be ways to sort of develop these things more quickly, to procure things somewhat faster. But if you have a decade long process, that’s--we're supposed to have long time horizons, but the time horizons are not that long.

Josh Wolfe: The one thing I will add that I think is a tremendous testament to both those companies, and Anduril, and others that are fast growing and now have momentum, is the people that are attracted to high growth, really big historic narratives. And so if you think about the flow of talent, the flow of human capital, the flow of financial capital, they don't want to go into these small hot dog stands or these $30mn businesses, but when you see people voting with their feet, and I in no way mean to offend any of the primes who do incredible work, but many of the top engineers are saying, I don't want to go to, for example, Lockheed, which is one of my investors--they want to go to some of these high growth early companies where they see the opportunity to create a fortune in the future as much more attractive.

…

Josh Wolfe: I think Mike makes a great point in the liaison role that he's playing for some of the emerging technology companies and DoD. And it's a really critical one, because it helps to reduce, not eliminate, but reduce a very key risk, which is market risk. So if you think about all the risks--I mean, we have national risks, be it China, Russia, non-state actors, and you have warfighters that want technology, and then you have investors that are willing to take the risk to fund that technology. We're thinking about people risk--are we backing the right people? Technology risk--will the thing work? Competition. But a key risk is market. And you will have a lot of venture capitalists that say, Oh, you're focused on the defense industry. Okay, what are the stereotypes? Obviously stereotypes have elements of truth--it’s slow-moving, it's bureaucratic, it's very political. They might not pick the best technology--they're going to give it to this prime that they've been working with for 20 years. And so whatever you can do to eliminate that risk--it's sort of like, as a country, we're fighting with ourselves by not equipping the warfighters with the absolute best technology that is coming from some of these early companies.

On the Shift in Global R&D Spending

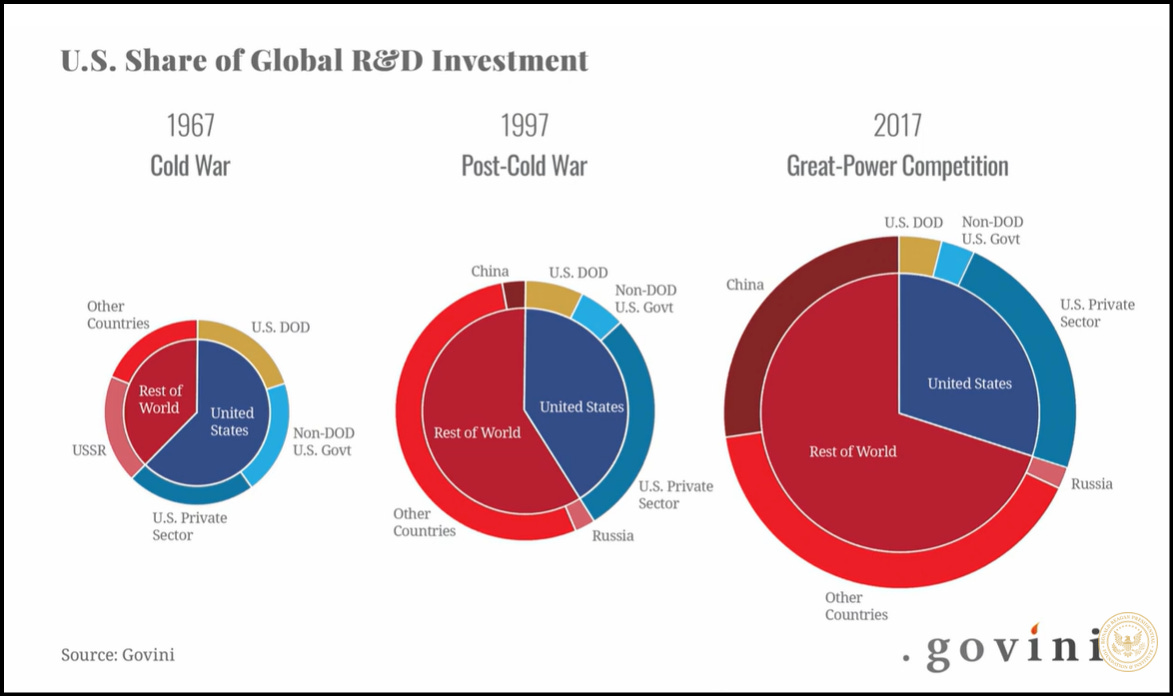

Host: All right, I want to bring up a graphic here.

Host: I actually cited this on TV yesterday, too, because I think it's a really--I think it's a really interesting graphic. This is from Govini. This is the US share of global R&D investment, 1967, as you can see right here. It was a little over 60%. A big chunk of that was DoD related. Obviously the USSR also made up a significant size of the global total. And as you see it move through the next several decades and over the next 50 years, you get to 2017, and the US is less than 30% of global R&D spending. And look at what's happened with China. It's completely--it's jumped, and it's become a larger share of the global total than the USSR was during the Cold War. We were having this question before we got on stage, and Peter, I'll send it back over to you. How much is the need for new innovation, new technologies, the way you're thinking about funding companies and starting companies right now? How much is that being driven by the China discussion?

Peter Thiel: Well, I think the China dynamic has changed things tremendously in the last few years, where in the 90s and maybe still in the 2000s, we thought the Cold War was over and there was sort of a way we could proceed on where it could be slower, you could go with the bigger primes, things like this. I think China is going to force us to compete, to think much harder how we can deploy technologies much faster. And so I think it's just--it's changed the dynamic tremendously. I think we have a serious space race with China. We have a serious AI race. I've complained in the past about Google's--what I think--very problematic decision to pull out on Project Maven, the AI project with the US military, and to continue to work with China, which I think is sort of a shocking, unprecedented thing for a major American company not to work with the US but indirectly to work with our geopolitical rival’s military. But I think sort of the silver lining of the Maven controversy is that it tells us that AI is a military technology--or at least it's a dual use technology. And it's not something that Silicon Valley had acknowledged for a long time. I think it's very different when you think about the debate we had about nuclear weapons in the 1940s, where it was clear it was dual use, and you had a debate, and there were scientists like Oppenheimer who were against, and Teller were in favor, and you had sort of a debate. And we haven't had this debate. And I think even though I disagree with Google on Project Maven, I think it has forced a debate. And that sort of debate about AI is going to happen in many other areas of technology. They are dual use, and it’s--we better make sure we get the cutting edge ones on our side.

Host: Do you think Silicon Valley or the rest of Silicon Valley has woken up to that fact? Do you think that's a Google specific situation, or do you think it's a bigger, broader issue debate? It's certainly been framed around this idea of ethics, for example, employees not wanting to work on military related projects. Do you think it's Google-specific or do you think it's more of a bigger, broader culture?

Peter Thiel: There are things that are specific to Google, there are things that are more general in Silicon Valley where it has sort of--it's very disconnected from the history of the 1950s and 1960s where Silicon Valley was heavily created by military R&D, and people are just not aware of that history in any way. I think the Seattle companies, Amazon, Microsoft, are probably somehow better than the Silicon Valley companies on this. So there's some cultural differences between Seattle and Silicon Valley. But even in Silicon Valley, you talk to people, and there is sort of a recognition that something's very different. I would push back on the ethical framing. I think that when it's a choice between the US and China, it is always the ethical decision to work with the US government. And even though we don't know all the unethical things that are going in China, they're sort of often hidden and obscured, that's a much more problematic ethical one. And so it's really odd that we're having any sort of debate where that's even framed as a question.

Josh Wolfe: Silicon Valley has this mythology of being a bunch of fruit orchards and then suddenly Hewlett Packard gets formed in a garage. But the origins of Silicon Valley were in electronic warfare and defense. And I do think, while it's not necessarily ethics in many cases, that there is an aversion for people to want to work on defense-related things, and that is a zeitgeist that is growing. I do think an element of that is some of the companies pandering to the lowest common denominator and wanting to avoid HR issues and controversies. But I think another part of this, and this is a conversation I had with Brigadier General Braga in Paycom, in Thailand, the Philippines. The idea that in the 80s, when I was growing up, we had a clear and present danger in Soviet Russia. And it was a narrative that rallied people together, and it was everywhere. I watched WWF wrestling, you had Hulk Hogan and you had Nikolai Volkov, you had Rocky and you had Drago, you had Red Dawn and--

Host: Great movie, by the way.

Josh Wolfe: Today, you would be hard pressed if find a Chinese villain. And some of that is for economic reasons. Hollywood does not want to insult one of its biggest markets. And some of it is ownership and other acquisition decisions that China has made quite strategically. But that affects the narrative and the zeitgeist of young people growing up in the country and the things that they value. And the good thing--I think in the 80s and early 90s, you had an influx of Russian immigrants that were so pining to be American that so wanted to raise the American flag and be part of it--there was no question of them going back to their country. And now I think there's a big influx of immigrants that either they're not welcome here, which is a problem, or they go back and the transfer of intellectual property and knowledge is very porous. And I think that there's a job society can do in sort of the information ops of retelling a narrative that can bind people and galvanize some of our best and brightest who want to work on American defense.

…

Josh Wolfe: And we went from Vannevar Bush to being warned of a military industrial complex. And there was an aversion for that in commerce circles. But China is a military industrial complex. And the point about the reach, I mean, I banned a year and a half ago TikTok as an app in my house because I just knew that my kids, three kids, are going to be using it, and facial recognition, everything is going back to the CCP.

On Liquidity for Defense Investments

Host: All right, so one of the other things I didn't mention earlier, but in terms of VC Investment 101, liquidity event, an exit, is basically how you realize gains in an investment. So that could be a share purchase, acquisition, or takeover. It could also be a company going public, an IPO, direct listing increasingly becoming part of the conversation as well--Peter, I'll put this question to you. Given the fact that we do have some, albeit just a couple, but some startups starting to take on more of this national security business, we're certainly seeing companies that are staying private for longer, but whether it's Space X, whether it's Palantir, which was started in 2004, are these companies, or Palantir specifically, is this a company that will go public? And I guess, is the timeframe in terms of one of those exit strategies the same, or is it elongated, when you're talking about defense?

Peter Thiel: I think it’s super elongated in Silicon Valley generally at this point. This is sort of the enormous shift that happened after the 1990s, where the 1990s in the dotcom bubble, everyone tried to take companies public, put them on the stock market as fast as possible. And then in the aftermath, you want sort of very profitable businesses that are at significant scale. There's a lot more regulation around having a public company. And so I think there's sort of--I think in general, it has gotten elongated tremendously. It's probably not quite as urgent for companies to go public. There's plenty of capital available in the private markets to fund these companies over the years. But yes, there's--for both SpaceX and Palantir, there's ultimately some kind of IPO exit at some point in the future. You can create liquidity programs for early investors, for employees so it's not as though everybody's had to hold the shares for 15 years since the company was started in 2004. But I think--I always think one of the challenges with taking companies public is that you can sort of--it's always this danger in a tech company for it to become overly bureaucratized. And in a public company, the accounting people, the legal people become far more powerful. And you can sort of think of it as like sort of a coup by the accountants and the lawyers. And so if you're still like, innovating very fast and very hard, you may want to try to defer the point at which that coup takes place.

Host: Josh, I'll put the same question to you. How do you think about it as an investor in these types of companies?

Josh Wolfe: Liquidity. We want it.

Host: Okay.

Josh Wolfe: No, I mean, I think there's a--typically, by the way, venture capital funds are 10 years. So I actually think that there's lots of different advantages you can have as an investor. You can have an informational advantage. I know something that you don't know. That's very hard when there's so many smart people. I can have an analytical advantage. Peter and I both look at the same piece of information, he analyzes it better than I do. He's got an analytic advantage. Also very hard with both computers and really smart people. But the one real edge you can have as an investor is a behavioral one. And I'm going to make an analogy in a moment how I think this applies to military as well. But for us, that means having a longer time horizon, what we call time arbitrage, than the average investor. And so if the average investor is looking at the the dotcom or the ecommerce marketplace that's going to give them a signal that this is going to be a success in a year or two, and we're looking at something that might not give us a signal for four or five or six years, by definition, there are going to be fewer investors looking to fund the very thing that we're funding. And so the valuations of those things will be lower. And if we are right, the returns for our investors and us will be higher. So we like to actually look at things that are further out, which also means that they're riskier and more improbable to work. But when they do, we expect that they're going to work in a really big way. The analogy I was going to make to the military is in the same regard, taking those long-term views, but being able to think about technologies that are early today, being developed by these cutting edge engineers, that can really give again technological advantage. And so, just observing, in theater, and at Air Force bases, I've seen people that can paint a laser target in five seconds on the ground, and it takes five minutes--five minutes--for them to save an email, because of the classification systems that they have, and the IT that's so outdated. I've seen a B2 bomber at Whiteman Air Force Base, and sat inside and watched as we got a blue screen of death from Windows NT that was operating it. Like I was floored. And so part of me was very scared. And I did a briefing at the Pentagon and I said, If I was actually a mal-intent, a mean-spirited, negatively-intented adversary, I would actually plant inside the Pentagon an IT operations director that basically has the exact system that you guys have today as a means of sabotage. And it was scary. And I think if--and this is one of the things that Mike is doing--but if you get more people from the Pentagon coming to Silicon Valley and seeing the speed at which people operate, the speed at which information flows, the systems and how agile they are, I think they will look with envy and say, My God, how are they able to do that? And I think that that will lead to faster adoption, which again will lead to faster adoption of technologies that will give advantage.

On Defense Spending

Peter Thiel: So I think--just coming back to the R&D chart you had earlier, I don't think it's necessary for the US military to go back to doing 30% of the R&D spend globally. But if we're not going to do that, we have to reform the procurement process. So it's okay for us to outsource the part of the R&D to venture capital, to Silicon Valley, to other parts of the private sector. But that's only going to work if the procurement process gets reformed, and then there's a pathway for this to happen. There's no shortage of venture capital, generally. We live in a world where central banks have been printing money for 10 years. We have $20tn of bonds that have negative yields. There's no shortage of venture capital. But there is not that much being put into sort of military defense companies because we all have this look-ahead function where it's going to be slow. If it's dual use, well, we better focus on the commercial, we don't know how fast the military will happen. And it's like always this race, and if you can get something in six months on the commercial side, the military side might take three years. Even if you get it down to two years, you're still going to focus on the commercial side. And so there's all--so I think Silicon Valley, it's not just ideological or myopic. There is a certain part of it where it's a rational, look ahead function that people have.

Other Panelist: I just want to add, though, to the point Peter's making--there's been a lot of work done on procurement. So I think the work that needs to be done now is on budgeting. And this is where Congress comes into play. So there's a lot more flexibility than is known on the procurement side, and DIU is an example of that--we use something called other transaction authority. So we can move faster on the procurement. But if you don't have the budget in place, there are no dollars from the comptroller moving to say you can do that.

Host: Josh, you looked like you wanted to--

Josh Wolfe: No, I was just going to say in both cases that speed is an advantage. And whether it's the flow of money or it's the ease of procurement, we can just be massively advantaged by removing the friction in both those processes. And importantly, because what Peter said is really important, the incentive is there from private capital. We are roaring to put more money to work. The incentive is there from the entrepreneurs and the engineers. They are roaring to develop and to serve military--in some cases exclusively military. They're totally comfortable doing that. The incentive has to be there from the government to say we want to pull this stuff through so that we can be advantaged and doing it with as least friction as possible.

On M&A in the Defense Industry

Host: All right, I know we're going to be opening this up to Q&A here, so I'm just going to take that. Thank you. All right, we've got a couple questions here. Let's see if we can get through them all. Could larger traditional defense primes just acquire startups--oh, this is a good question--to harness their tech and human capital, much like other big tech companies such as Google do with startups?

Josh Wolfe: They certainly could, but in some cases, the entrepreneurs have grander ambitions. And there's a lot of people that don't want to sell to Facebook or don't want to sell to a Lockheed or a Raytheon because they think that their job isn't done and they've got another 10 years to grow and they want the freedom to do that. So in some cases it does make sense. But in other cases, I think the most ambitious entrepreneurs are going to stay private and we should give them the capital and the runway to take off.

Peter Thiel: There's always--there are all these advantages larger scale companies have. When I started PayPal years ago, very different context--I was always asked, Why can't a big bank just do this? And I never had a good answer to that. Because in theory, the banks have scale, they can have longer time horizons, they have more capital, they have a lot of talent. And I think the general answer is that it's just the internal politics are unbelievably bad. And this is true not just of large parts of the government, it's also true of a lot of large corporations become incredibly politicized in ways that are not good for innovation. So I think you can acquire a technology company at that point where you don't need to innovate anymore. So if it's a fully formed thing, maybe that's a point at which it makes sense for the primes to acquire them, but if you still need to maintain that culture of innovation, that's going to be very hard to do.

Josh Wolfe: Follow the people. You know the old quote from Walter Wriston, Capital goes where it's welcome and stays where it's well treated. Think of that of human capital too. Rarely do I ever hear in a high growth, successful, or succeeding company, This thing is just moving too fast for me. I really want to go into a slower moving thing. But so often I have resumes coming in from big companies where people are saying, It's just really frustrating, and it’s so political, and I just want something fresh and exciting. So it is the politics.

On the Effect of Government Regulations Limiting Profit

Host: All right, we've got one more question, and we got one more minute. So here we go. How did government interests and IP rights and government regulations limiting profit impact venture capital?...Want me to read it again?

Peter Thiel: Yeah, I wouldn't say that's the main--I think the biggest problems are the ones we've talked about, which is just: procurement, budgeting, a fast way to ramp up and scale these businesses. And if we solve those, we will have solved the vast bulk of the challenges we have.

Josh Wolfe: And making concentrated, big bets. I mean, that's what we do. We make big, concentrated bets. It's okay to make a few bets, but then once you see something is going to take off, really put the heft behind it and give it the push, particularly if we're going to discourage foreign capital from coming in. I think it's absolutely imperative.

If you got this far and you liked this piece, please consider tapping the ❤️ above or sharing this letter! It helps me understand which types of letters you like best and helps me choose which ones to share in the future. Thank you!

Wrap-up

If you’ve got any thoughts, questions, or feedback, please drop me a line - I would love to chat! You can find me on twitter at @kevg1412 or my email at kevin@12mv2.com.

If you're a fan of business or technology in general, please check out some of my other projects!

Speedwell Research — Comprehensive research on great public companies including Constellation Software, Floor & Decor, Meta (Facebook) and interesting new frameworks like the Consumer’s Hierarchy of Preferences.

Cloud Valley — Beautifully written, in-depth biographies that explore the defining moments, investments, and life decisions of investing, business, and tech legends like Dan Loeb, Bob Iger, Steve Jurvetson, and Cyan Banister.

DJY Research — Comprehensive research on publicly-traded Asian companies like Alibaba, Tencent, Nintendo, Sea Limited (FREE SAMPLE), Coupang (FREE SAMPLE), and more.

Compilations — “An international treasure”

Memos — A selection of some of my favorite investor memos

Bookshelves — Collection of recommended booklists.